Thoughts on The Debt Ceiling Impasse

The United States reached its borrowing limit (debt ceiling) back on January 19, and the Treasury Department estimates that unless the limit is raised, the government will run out of money in early June. In short, the U.S. spends more than it takes in and depends on borrowing to bridge the gap. Without the ability to borrow further, the government will be unable to fully fund the obligations to which Congress has already committed. These include things like Social Security, Medicare, tax refunds, and interest owed on existing debt obligations.

Congress has lifted the debt ceiling 45 times over the past 40 years, often with little fanfare. This time however there is an impasse where Republicans have included spending cuts in legislation that increases the debt limit while the White House has said it would not accept any conditions. If the impasse is protracted, it raises the possibility of a partial government shutdown and the U.S. defaulting on its debt. This could result in widespread economic damage at home and globally at an already-precarious time for the US and global economy.

Given the headlines and broad concern, we want to share how we take into account the debt ceiling impasse in our investment thinking. Looking out longer-term, from a portfolio management and investment standpoint we don’t believe today’s debt ceiling stalemate will cause any permanent or medium-to-longer-term damage to financial markets, corporate fundamentals, or the economy. Rather, it remains a highly uncertain short-term event: a known unknown.

We can look at history and see that politicians have played this game of “chicken” before and ultimately compromised and passed a new debt ceiling each time. But what is different this time is the level of acrimony between Democrats and Republicans. So, while we are confident it will get resolved, we have much less confidence about the timeline for resolution and the potential for shorter-term consequences that could result.

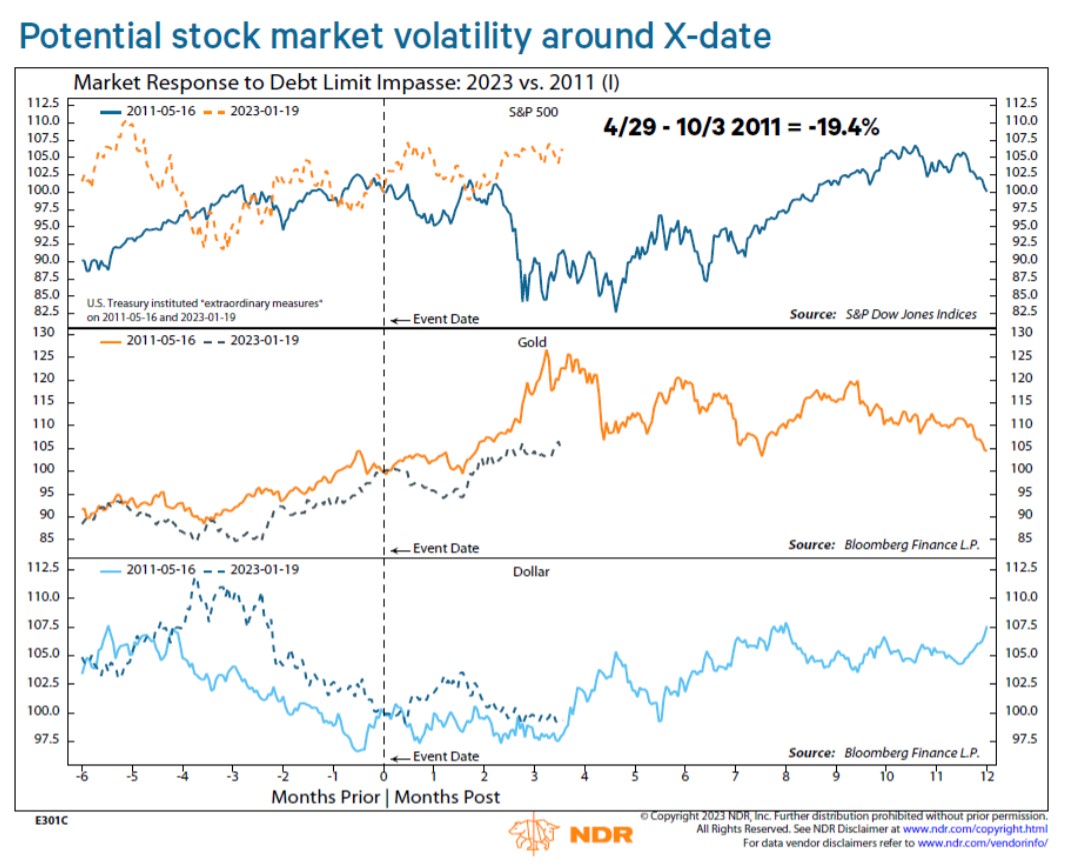

From an investment standpoint, we are aware of and prepared for a reasonable worst-case shorter-term scenario, where financial markets (and risk assets like stocks) sell off on fears that a government shutdown and/or default will trigger a sharp economic disruption. Ned Davis Research notes that in the 2011 debt ceiling standoff, the S&P 500 dropped nearly 20% between April 29 and October 3, which included the X-date (aka the date at which the government runs out of money) of August 2. See their chart below shows how 2011 unfolded with an overlay showing this year to date.

This strikes us as a reasonable worst-case downside for this time around too. As we know, the economy is already in a precarious situation, based on leading indicators and tight monetary policy. A debt ceiling crisis could push us into recession or raise investors’ fears of such (which in turn could become self-fulfilling).

Not surprisingly for those who know how we invest, we are not making any portfolio changes in reaction to the debt ceiling standoff. Doing so successfully would require that we have knowledge not yet reflected in market prices about what is going to happen over the coming months. While we have views and opinions, we do not have a level of confidence sufficient to justify making bets on our (or anyone else’s) views given the inherent uncertainty of people and politics.

Our base case assumption is that the most likely outcome is not a worst-case scenario; that the two sides will reach an agreement or another workaround can be found that avoids a crisis outcome. But if there is a crisis outcome and stocks drop in the neighborhood of 20% as they did in 2011, we would consider adding to our U.S. equity allocation, which is currently underweight. The reason we would add to stocks is that we expect such a decline would be followed by a recovery, and buying at prices roughly 20% below today’s, the U.S. stock market could look quite attractive over the next five to 10 years. The same is true of any unpredictable shocks that create fear and cause stocks to drop in the short term. History shows it pays to be a buyer during such periods (or at least a holder) and not a seller.

As we know, investors who own equities in their portfolios must be prepared to ride through short-term disruptive and discomforting periods, in order to earn the longer-term higher returns stocks have historically generated.

If you have any questions or concerns about your situation, please do not hesitate to reach out.

{kind=link}